Blog

Stock written off tax deductible

Stock written off tax deductible

Issue

Whether the stock written off need to add back in tax computation? in what circumstances have to add back?

Fact

According to PR 2/2020, this ruling explains that if it is an actual write-off of stock in trade, then it is deductible. If it is just a provision for obsolescence of stock in trade, it will need to add back to tax computation.

Tax opinion

If it is an actual write-off of stock in trade that is charged to the profit and loss account is allowable for tax-deductible. If it is a provision for obsolescence of stock in trade, it will need to add back in tax computation.

Source

Public Ruling 2/2020 tax treatment of stock in trade part 1 – valuation of stock

https://phl.hasil.gov.my/pdf/pdfam%20PR_02_2020.pdf

Visit Us

-

Wisma KTP, 53 Jalan Molek 1/8, Taman Molek, 81100 Johor Bahru

-

Wisma THK, 41, Jalan Molek 1/8, Taman Molek, 81100 Johor Bahru

KTP (Audit, Tax, Advisory)

An approved audit firm and licensed tax firm operating under the KTP group based in Johor Bahru providing audit, tax planning, advisory and compliance services to clients

-

Website www.ktp.com.my

-

Instagram https://bit.ly/3jZuZuI

-

Linkedin https://bit.ly/3sapf4l

-

Telegram http://bit.ly/3ptmlpn

THK (Secretarial, Account, Payroll, Advisory)

A licensed secretarial firm in Johor Bahru providing fast reliable incorporation, secretarial services, corporate compliance services, outsource booking, accounting and payroll services to clients

-

Website www.thks.com.my

-

Facebook https://bit.ly/3nQ98rs

KTP Lifestyle

An internal community for our colleagues on work and leisure.

-

Tiktok http://bit.ly/3u9LR6Q

-

Youtube http://bit.ly/3ppmjyE

-

Facebook http://bit.ly/3ateoMz

-

Instagram https://bit.ly/3jZpKLo

KTP Career

An external job community on vacancy in Johor Bahru for interns, graduates & experienced candidates.

-

Instagram https://bit.ly/3u2PxHg

-

Facebook http://bit.ly/3rPxz9o

#Ktp #Thks

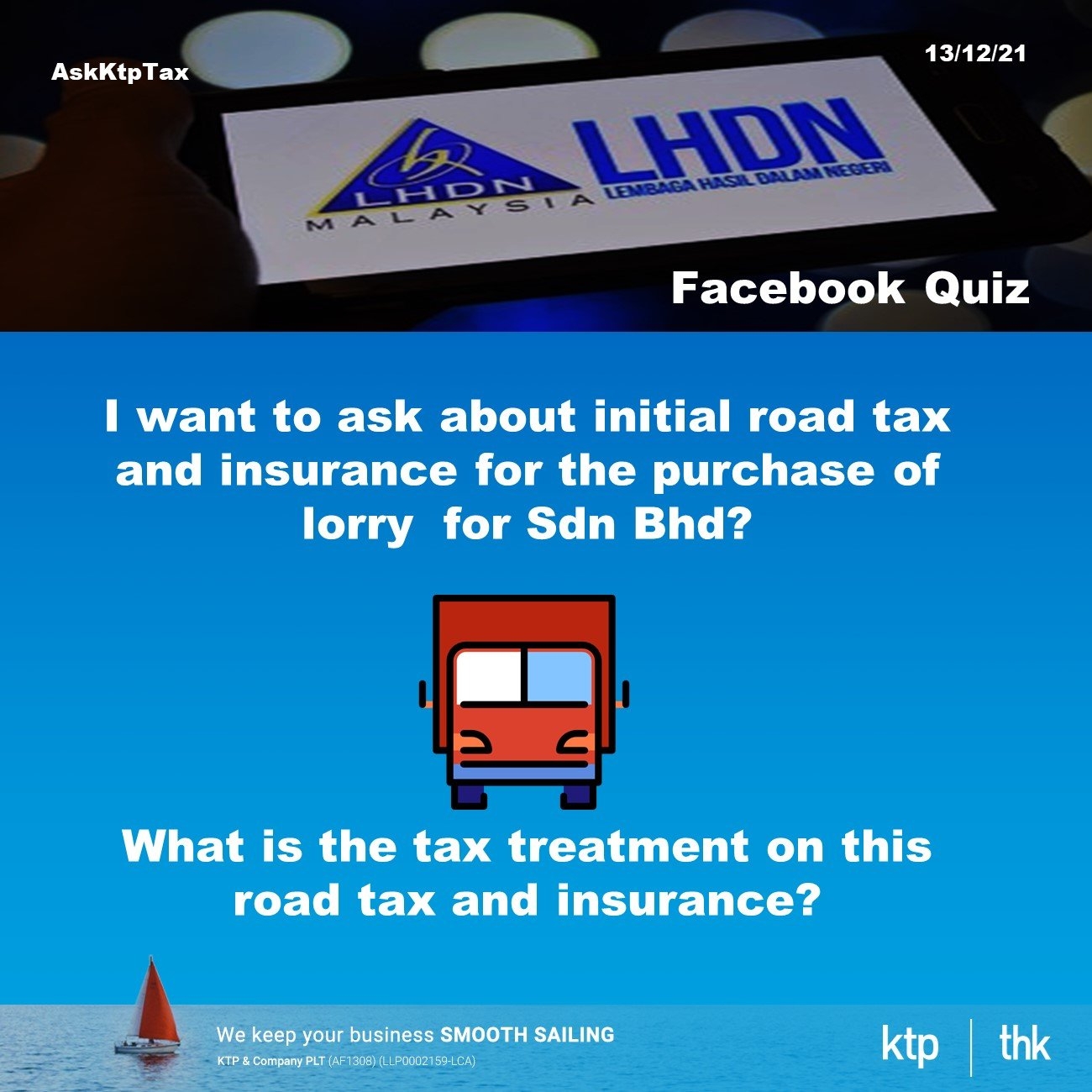

Upkeep of motor vehicle tax treatment

Upkeep of motor vehicle tax treatment

Issue

For the purchase of a new non-commercial motor vehicle for a company, specifically, a lorry, is initial insurance and road tax-deductible as expenses or need to add back as capital in nature?

Fact

1. According to PR 6/2015 #5.2, Expenditure in respect of the vehicle which does not qualify for capital allowance claim is as follows:

(i) road tax, insurance and hire purchase interest does not qualify for capital allowance as the expenditures are recurring expenses which allowable as expenditures under subsection 33 (1) of the ITA.

2. Under subsection 33(1) of the ITA, an expense wholly and exclusively incurred in the production of gross income from a source is allowable as a deduction against gross income from that source. As long as the lorry is used for business purposes wholly and exclusively, the expenses incurred are tax deductible.

Tax opinion

Road tax and insurance do not qualify for capital allowance. However, they can be deductible as expenses as this is recurring expenses which is allowable as expenditure under subsection 33(1) of the ITA.

Source

1. Public Ruling No. 6/2015 : Qualifying expenditure and computation of capital allowances

https://phl.hasil.gov.my/pdf/pdfam/PR_6_2015.pdf

2. Income Tax Act 1967 – Section 33(1) Adjusted income generally

https://phl.hasil.gov.my/pdf/pdfam/Act_53_20190101.pdf

Visit Us

-

Wisma KTP, 53 Jalan Molek 1/8, Taman Molek, 81100 Johor Bahru

-

Wisma THK, 41, Jalan Molek 1/8, Taman Molek, 81100 Johor Bahru

KTP (Audit, Tax, Advisory)

An approved audit firm and licensed tax firm operating under the KTP group based in Johor Bahru providing audit, tax planning, advisory and compliance services to clients

-

Website www.ktp.com.my

-

Instagram https://bit.ly/3jZuZuI

-

Linkedin https://bit.ly/3sapf4l

-

Telegram http://bit.ly/3ptmlpn

THK (Secretarial, Account, Payroll, Advisory)

A licensed secretarial firm in Johor Bahru providing fast reliable incorporation, secretarial services, corporate compliance services, outsource booking, accounting and payroll services to clients

-

Website www.thks.com.my

-

Facebook https://bit.ly/3nQ98rs

KTP Lifestyle

An internal community for our colleagues on work and leisure.

-

Tiktok http://bit.ly/3u9LR6Q

-

Youtube http://bit.ly/3ppmjyE

-

Facebook http://bit.ly/3ateoMz

-

Instagram https://bit.ly/3jZpKLo

KTP Career

An external job community on vacancy in Johor Bahru for interns, graduates & experienced candidates.

-

Instagram https://bit.ly/3u2PxHg

-

Facebook http://bit.ly/3rPxz9o

#Ktp #Thks

KTP | THK Investment Club 2022/2023

KTP | THK Investment Club 2022/2023

Greetings!

Warren Buffet once quoted: Never depend on single income, make investment to create a second source.

We are delighted to introduce our KTP | THK Investment Club Committee for 2022/23.

Composition of the committee

It is led by our AM Arthur and comprises our colleagues Chris. More members will be joining the committee as the time comes.

Our Group Principal Mr Koh Teck Peng will be the mentor of this committee.

The Objectives

KTP | THK Investment Club Committee aims on learning and making money :

1. Organise learning events to invest in stock based on Value Investment methodology

2. A platform to evaluate stock based on Value Investment principles

3. Sharing of investment experience from our mentor Mr Koh Teck Peng

4. Invest in cryptocurrency

5. & etc.

Pre-conditions of joining the Investment Club

1. Open a CDS account with Bursa Malaysia

2. Open a Luno/Tokenize for cryptocurrency investment

Let us guide you to lead a better prospect investment life where it will change your future for a greater purpose.

Visit Us

-

Wisma KTP, 53 Jalan Molek 1/8, Taman Molek, 81100 Johor Bahru

-

Wisma THK, 41, Jalan Molek 1/8, Taman Molek, 81100 Johor Bahru

KTP (Audit, Tax, Advisory)

An approved audit firm and licensed tax firm operating under the KTP group based in Johor Bahru providing audit, tax planning, advisory and compliance services to clients

-

Website www.ktp.com.my

-

Instagram https://bit.ly/3jZuZuI

-

Linkedin https://bit.ly/3sapf4l

-

Telegram http://bit.ly/3ptmlpn

THK (Secretarial, Account, Payroll, Advisory)

A licensed secretarial firm in Johor Bahru providing fast reliable incorporation, secretarial services, corporate compliance services, outsource booking, accounting and payroll services to clients

-

Website www.thks.com.my

-

Facebook https://bit.ly/3nQ98rs

KTP Lifestyle

An internal community for our colleagues on work and leisure.

-

Tiktok http://bit.ly/3u9LR6Q

-

Youtube http://bit.ly/3ppmjyE

-

Facebook http://bit.ly/3ateoMz

-

Instagram https://bit.ly/3jZpKLo

KTP Career

An external job community on vacancy in Johor Bahru for interns, graduates & experienced candidates.

-

Instagram https://bit.ly/3u2PxHg

-

Facebook http://bit.ly/3rPxz9o

#Ktp #Thks

2022年预算案 (Free: 线上教导- 简化转让定价文件)

2022年预算案 (Free: 线上教导- 简化转让定价文件)

财政部长于10月29日在国会下议院提呈2022年财政预算案。由于疫情对经济造成的严重创伤仍显现,为了引导国家走向经济复苏,本次财政预算案分为三大主轴;加强复苏、建立经济韧性和推动革新。

想知道这次的预算案对你的业务有什么帮助或者影响吗?欢迎加入KTP | THK 预算案研讨会,我们将会跟大家概述2022年预算案中最主要的税务更新与改变。

Bonus:免费教导简化转让定价文件 (Limited/Simplified/Minimum transfer pricing documentation)

课程内容:

-

第 1 节:2022 年财政预算案—其改变和对纳税人的影响

-

第 2 节:准备简化转让定价文件。

2022年预算案课程

-

Subject : 2022年预算案 (Free: 线上教导- 简化转让定价文件)

-

Date : 20.12.2021

-

Time : 10:30 am to 12:00 pm

-

Venue : Zoom

-

Fee : 免费

-

Language : 中文

-

Registration link (仅开放 KTP|THK 现有客户) : https://bit.ly/31uTpYp

Visit Us

-

Wisma KTP, 53 Jalan Molek 1/8, Taman Molek, 81100 Johor Bahru

-

Wisma THK, 41, Jalan Molek 1/8, Taman Molek, 81100 Johor Bahru

KTP (Audit, Tax, Advisory)

An approved audit firm and licensed tax firm operating under the KTP group based in Johor Bahru providing audit, tax planning, advisory and compliance services to clients

-

Website www.ktp.com.my

-

Instagram https://bit.ly/3jZuZuI

-

Linkedin https://bit.ly/3sapf4l

-

Telegram http://bit.ly/3ptmlpn

THK (Secretarial, Account, Payroll, Advisory)

A licensed secretarial firm in Johor Bahru providing fast reliable incorporation, secretarial services, corporate compliance services, outsource booking, accounting and payroll services to clients

-

Website www.thks.com.my

-

Facebook https://bit.ly/3nQ98rs

KTP Lifestyle

An internal community for our colleagues on work and leisure.

-

Tiktok http://bit.ly/3u9LR6Q

-

Youtube http://bit.ly/3ppmjyE

-

Facebook http://bit.ly/3ateoMz

-

Instagram https://bit.ly/3jZpKLo

KTP Career

An external job community on vacancy in Johor Bahru for interns, graduates & experienced candidates.

-

Instagram https://bit.ly/3u2PxHg

-

Facebook http://bit.ly/3rPxz9o

#Ktp #Thks

LHDN Personal Tax Relief 2021

Malaysia Personal Tax Relief 2021

As we know time is left until the Year 2022 is around 3 weeks and it is almost over!

That’s mean it is time for us to rummage through our house, looking for the receipts!

You can decide the tax saving for your personal tax granted by Lembaga Hasil Dalam Negeri (LHDN).

So, do not miss out on any claim! Here is a complete tax relief checklist at a glance.

Click Personal Tax Relief Year 2021

Remember

you must keep your receipts properly as evidence to avoid any penalty imposed by LHDN!

Source:

Public ruling 5/2021 Taxation Of A Resident Individual Part I - Gifts Or Contributions And Allowable Deductions

https://phl.hasil.gov.my/pdf/pdfam/PR_05_2021.pdf

Visit Us

-

Wisma KTP, 53 Jalan Molek 1/8, Taman Molek, 81100 Johor Bahru

-

Wisma THK, 41, Jalan Molek 1/8, Taman Molek, 81100 Johor Bahru

KTP (Audit, Tax, Advisory)

An approved audit firm and licensed tax firm operating under the KTP group based in Johor Bahru providing audit, tax planning, advisory and compliance services to clients

-

Website www.ktp.com.my

-

Instagram https://bit.ly/3jZuZuI

-

Linkedin https://bit.ly/3sapf4l

-

Telegram http://bit.ly/3ptmlpn

THK (Secretarial, Account, Payroll, Advisory)

A licensed secretarial firm in Johor Bahru providing fast reliable incorporation, secretarial services, corporate compliance services, outsource booking, accounting and payroll services to clients

-

Website www.thks.com.my

-

Facebook https://bit.ly/3nQ98rs

KTP Lifestyle

An internal community for our colleagues on work and leisure.

-

Tiktok http://bit.ly/3u9LR6Q

-

Youtube http://bit.ly/3ppmjyE

-

Facebook http://bit.ly/3ateoMz

-

Instagram https://bit.ly/3jZpKLo

KTP Career

An external job community on vacancy in Johor Bahru for interns, graduates & experienced candidates.

-

Instagram https://bit.ly/3u2PxHg

-

Facebook http://bit.ly/3rPxz9o

#Ktp #Thks

Xero Bronze Partner

Account job near Johor Bahru

拒绝平凡...加入我们

你是否常常在问你自己 ?

1. 跟对了目前老板?

2. 跟对了公司?

3. 厌烦你目前的工作?

4. 没机会发挥的长处?

KTP是间有20年++ 中小型会计楼, 俗称 ”𝐚𝐜𝐜𝐨𝐮𝐧𝐭𝐢𝐧𝐠 𝐟𝐢𝐫𝐦”, 急需一位积极, 认真, 诚信度与公司的配合度高, 懂得使用电脑SQL, Xero, Audit Express, BrassTax 系统. 五天制. 精通中, 英书写及对话. 吸收能力强的人才.

𝐀𝐜𝐜𝐨𝐮𝐧𝐭 𝐀𝐬𝐬𝐨𝐜𝐢𝐚𝐭𝐞

基本条件:

📌欢迎有相关会计工作经验或相关文凭者申请

📌提供在职培训

📌勤劳肯学

📌有使用SQL,XERO accounting software经验者优先,但是不是必须的

📌会基本的中,英,巫文

📌能即刻上班者为佳

𝗔𝘂𝗱𝗶𝘁 𝗔𝘀𝘀𝗼𝗰𝗶𝗮𝘁𝗲

基本条件:

📌需有会计相关的专业文凭,或金融/或相关领域的学士学位

📌做事认真严谨、有较强的学习能力&沟通协调能力

📌欢迎毕业🎓生

📌通晓英,华,巫文

为何加入我们?

📌免费提供专业培训

📌给你一个完全没有office politics 的环境,让你开开心心工作🥰

📌给你work life balance的理念,让你玩的时候尽力玩

📌公平的薪金制度

有意者请发你的履历表至:𝗰𝗮𝗿𝗲𝗲𝗿𝘀@𝗸𝘁𝗽.𝗰𝗼𝗺.𝗺𝘆

Visit Us

-

Wisma KTP, 53 Jalan Molek 1/8, Taman Molek, 81100 Johor Bahru

-

Wisma THK, 41, Jalan Molek 1/8, Taman Molek, 81100 Johor Bahru

KTP (Audit, Tax, Advisory)

An approved audit firm and licensed tax firm operating under the KTP group based in Johor Bahru providing audit, tax planning, advisory and compliance services to clients

-

Website www.ktp.com.my

-

Instagram https://bit.ly/3jZuZuI

-

Linkedin https://bit.ly/3sapf4l

-

Telegram http://bit.ly/3ptmlpn

THK (Secretarial, Account, Payroll, Advisory)

A licensed secretarial firm in Johor Bahru providing fast reliable incorporation, secretarial services, corporate compliance services, outsource booking, accounting and payroll services to clients

-

Website www.thks.com.my

-

Facebook https://bit.ly/3nQ98rs

KTP Lifestyle

An internal community for our colleagues on work and leisure.

-

Tiktok http://bit.ly/3u9LR6Q

-

Youtube http://bit.ly/3ppmjyE

-

Facebook http://bit.ly/3ateoMz

-

Instagram https://bit.ly/3jZpKLo

KTP Career

An external job community on vacancy in Johor Bahru for interns, graduates & experienced candidates.

-

Instagram https://bit.ly/3u2PxHg

-

Facebook http://bit.ly/3rPxz9o

#Ktp #Thks

Special Income Remittance Programme (PKPP) to Malaysian Residents

Special Income Remittance Programme (PKPP) to Malaysian Residents

IRBM media release on - Special Program (PKPP) on remittance of foreign income dated 16/11/21.

IRBM will issue frequently asked questions (FAQs) as well as guidelines relating to the PKPP to the public in due course.

IRBM encourages taxpayers to participate in this special program that is offered to update their tax position.

Key summary of the PKPP :

-

The implementation period of PKPP is from 1 January 2022 to 30 June 2022 (PKPP period).

-

A tax rate of 3% (gross) on income brought into Malaysia during the said period.

-

There is no audit review, investigation or penalty on income brought into Malaysia during the PKPP period.

-

All income brought into Malaysia will be accepted in good faith by IRBM.

-

Income must be brought into / remitted into Malaysia within the PKPP period.

-

Taxpayers must make a declaration to join the PKPP not later than 30 days after the expiry of the PKPP period.

-

Tax payments shall be made in accordance with the normal payment arrangements prescribed for the year of assessment 2022 or 2023 whichever is applicable.

-

PKPP does not involve income derived from Malaysia which is subject to tax for the year of assessment 2021 and subsequent years of assessment and is remitted into or brought back to Malaysia during the PKPP period.

KTP takeaways

IRBM will review and examine the information on income of the Malaysian tax residents kept overseas that has been received through the tax information exchange agreements with other countries after 30/6/22.

Based on the review, if IRBM found that Malaysian source income kept overseas has not been reported, additional assessment can be raised together with penalties.

Visit Us

-

Wisma KTP, 53 Jalan Molek 1/8, Taman Molek, 81100 Johor Bahru

-

Wisma THK, 41, Jalan Molek 1/8, Taman Molek, 81100 Johor Bahru

KTP (Audit, Tax, Advisory)

An approved audit firm and licensed tax firm operating under the KTP group based in Johor Bahru providing audit, tax planning, advisory and compliance services to clients

-

Website www.ktp.com.my

-

Instagram https://bit.ly/3jZuZuI

-

Linkedin https://bit.ly/3sapf4l

-

Telegram http://bit.ly/3ptmlpn

THK (Secretarial, Account, Payroll, Advisory)

A licensed secretarial firm in Johor Bahru providing fast reliable incorporation, secretarial services, corporate compliance services, outsource booking, accounting and payroll services to clients

-

Website www.thks.com.my

-

Facebook https://bit.ly/3nQ98rs

KTP Lifestyle

An internal community for our colleagues on work and leisure.

-

Tiktok http://bit.ly/3u9LR6Q

-

Youtube http://bit.ly/3ppmjyE

-

Facebook http://bit.ly/3ateoMz

-

Instagram https://bit.ly/3jZpKLo

KTP Career

An external job community on vacancy in Johor Bahru for interns, graduates & experienced candidates.

-

Instagram https://bit.ly/3u2PxHg

-

Facebook http://bit.ly/3rPxz9o

#Ktp #Thks

Deferment of CP204 CP500 Payment Budget 2022 Part 2

Deferment of CP204 CP500 Payment Budget 2022 Part 2

The Postponement of 6 instalments on Estimated Tax Payable (CP204) and Instalment Payment Scheme (CP500) will be given automatically to qualified taxpayers with the status of micro, small and medium enterprises (MSMEs or PMKS) from Jan 1 to June 30, 2022.

What if taxpayers don’t want the deferment?

Taxpayers want to maintain the current tax instalment scheme.

-

IRB is not required to be notified as qualified taxpayers are allowed to follow the original CP 204 or CP 500.

-

Any tax instalments paid during the deferment period will be treated as payments towards the tax instalments for those respective months and will not be allowed to be carried forward for settlement of tax instalments after the deferment period.

Tax estimation

No changes to existing eligibility to revise tax estimates in the 6th or the 9th month and the special 11th month revision (subject to existing conditions)

Tax penalty ?

The increase in taxes for late payment of instalments will not be imposed for instalments deferred during the deferment period

6 instalment deferment

The Inland Revenue Board (IRB) informed that qualified taxpayers are based on records or the latest Income Tax Statement Form received by the board.

CP 204 deferment

For CP204 payment, business criteria that qualify for the PMKS status are companies, cooperatives, trust bodies and limited liability partnerships with a paid-up capital of less than RM2.5 million for ordinary shares at the start of the basic period of an assessment year.

In addition, the entity’s gross business income of RM50 million or below for an assessment year.

The postponement of CP204 payment to the taxpayer who fulfils the criteria will be sent via registered email with HASiL (the IRB).

CP500 deferment

The IRB informed that the postponement of CP500 payment is allowed automatically to all taxpayers concerned for the 2021 assessment year payment (for the payable date of Jan 1, 2022) and the 2022 assessment year payment (for the payable dates of March 1, 2022 and May 1, 2022).

FAQ on deferment

Frequently asked questions (FAQ) on the postponement could be accessed via the link https://phl.hasil.gov.my/pdf/pdfam/SOALAN_LAZIM_PINDAAN_BAJET_2022_CP204.pdf and the public can contact the HASiL Recovery Call Centre (HRCC) at 03-8751 1000 for further information.

Visit Us

-

Wisma KTP, 53 Jalan Molek 1/8, Taman Molek, 81100 Johor Bahru

-

Wisma THK, 41, Jalan Molek 1/8, Taman Molek, 81100 Johor Bahru

KTP (Audit, Tax, Advisory)

An approved audit firm and licensed tax firm operating under the KTP group based in Johor Bahru providing audit, tax planning, advisory and compliance services to clients

-

Website www.ktp.com.my

-

Instagram https://bit.ly/3jZuZuI

-

Linkedin https://bit.ly/3sapf4l

-

Telegram http://bit.ly/3ptmlpn

THK (Secretarial, Account, Payroll, Advisory)

A licensed secretarial firm in Johor Bahru providing fast reliable incorporation, secretarial services, corporate compliance services, outsource booking, accounting and payroll services to clients

-

Website www.thks.com.my

-

Facebook https://bit.ly/3nQ98rs

KTP Lifestyle

An internal community for our colleagues on work and leisure.

-

Tiktok http://bit.ly/3u9LR6Q

-

Youtube http://bit.ly/3ppmjyE

-

Facebook http://bit.ly/3ateoMz

-

Instagram https://bit.ly/3jZpKLo

KTP Career

An external job community on vacancy in Johor Bahru for interns, graduates & experienced candidates.

-

Instagram https://bit.ly/3u2PxHg

-

Facebook http://bit.ly/3rPxz9o

#Ktp #Thks

My, Sharanya Vijayan, first day at work in KTP

My, Sharanya Vijayan, first day at work in KTP

Starting a new job is truly exciting, but we might also feel nervous ahead of our first day job. Even though I have been working for 14 years down the road, venturing to a newer job, never ceased to evoke my anxiety, well which induced my non-stop sneezing and sore throat since yesterday morning.

Surprised me as I used to have this only when I am entering the exam hall.

In the excitement and having a mixture of anxiety, I woke up at 5 am to have a cup of coffee and tried to compose myself by watching my all-time favourite “The Good Wife” – never failed to boost my day thou. And yes, a pep talk from my husband.

I enjoyed the journey coming to work and even though my house is a bit further from Taman Molek, seeing my husband’s happiness that I am going to grow with the company and learn more to enhance my ACCA, skills, and knowledge – Pasir Gudang Traffic is not going to break us at anyways.

My first step in KTP office

Upon arrival, after a small breakfast the nearby café, I felt the warm welcoming from Anissa ( the admin sweet girl ). I have seen Jothi virtually and many times have spoken over the phone, but to my amusement, I was not expecting a bubbly but informative person to guide me and the other intern girl called Christine. I enjoyed the most to do the vide greetings as I believe it’s a great way to have an ice breaking session.

Orientation @ KTP

I will not deny that I enjoyed getting all the policies’ warming up sessions, the ‘Dos’ and ‘Don’ts’ , the MSI setup as well accessing to the outlook, tutoring the SOPs, walking us the cultures, showing all the areas, the most prime : sharing her positive opinions about KTP.

Giving me some books ( The seven spiritual laws of success, FISH, Who moved my cheese ) and allocated me a task of reading them and do a summary ( either via video or writing ) – well that task surely amazed me more. As a devoted reader and blogger as well a conveyer of my reading and writing contents to others – I will not deny how much I am thrilled and at the same time how much it has amazed me about the KTP culture- the emphasizing the holistic knowledge growth amongst staffs.

For many years, me running the HR head ( as in general affairs and customer service ), it’s a nice feeling to be the other side after sometime to get tutored and educate about company’s policies, and me listening without any judgements or having a skeptical way of thinking that been guided by a young person ( younger than me ) – were more exciting.

Seeing her, shows me how much KTP has shaped her to be a better leader and enhanced her skills to be a great trainer too.

After settling down, going through all the systems ( before my lunch break ), I liked them a lot! Me being a detailed orientated individual and system follower as well policies’ maker along with employment handbook setter- KTP’s investment in these areas, is a great cushion to have a great working system.

More confidence of mine to excel in ACCA has been instilled and more enthusiasm been moulded to give my utmost best to KTP and grow with them.

My official meeting with the boss of KTP

As talking to Mr Koh at 2.00pm, listening to his objectives and motives: despite I spoke lesser as I was focused about listening to his contents – I can see how much he gives importance to critical thinking as well the enhancement importance he gives towards a positive driven working culture are very significant aspects that he expects to be adhered by all the staffs.

I would like to have my understandings to be polished by Mr Koh as per my opinion, he is a leader who wants his fellow members to be in the right directions at all times.

The humbles in me being more evoked and the curiosity of learning has been instilled in a larger scale now.

Happy to be part of this reputable organization.

PS : 1st assignment in KTP - a covid test

Visit Us

-

Wisma KTP, 53 Jalan Molek 1/8, Taman Molek, 81100 Johor Bahru

-

Wisma THK, 41, Jalan Molek 1/8, Taman Molek, 81100 Johor Bahru

KTP (Audit, Tax, Advisory)

An approved audit firm and licensed tax firm operating under the KTP group based in Johor Bahru providing audit, tax planning, advisory and compliance services to clients

-

Website www.ktp.com.my

-

Instagram https://bit.ly/3jZuZuI

-

Linkedin https://bit.ly/3sapf4l

-

Telegram http://bit.ly/3ptmlpn

THK (Secretarial, Account, Payroll, Advisory)

A licensed secretarial firm in Johor Bahru providing fast reliable incorporation, secretarial services, corporate compliance services, outsource booking, accounting and payroll services to clients

-

Website www.thks.com.my

-

Facebook https://bit.ly/3nQ98rs

KTP Lifestyle

An internal community for our colleagues on work and leisure.

-

Tiktok http://bit.ly/3u9LR6Q

-

Youtube http://bit.ly/3ppmjyE

-

Facebook http://bit.ly/3ateoMz

-

Instagram https://bit.ly/3jZpKLo

KTP Career

An external job community on vacancy in Johor Bahru for interns, graduates & experienced candidates.

-

Instagram https://bit.ly/3u2PxHg

-

Facebook http://bit.ly/3rPxz9o

#Ktp #Thks

Deferment of CP204 Payment Budget 2022

Deferment of CP204 Payment Budget 2022

The Postponement of Estimated Tax Payable (CP204) and Instalment Payment Scheme (CP500) will be given automatically to qualified taxpayers with the status of micro, small and medium enterprises (MSMEs or PMKS) from Jan 1 to June 30, 2022.

6 instalment deferment

The Inland Revenue Board (IRB) informed that qualified taxpayers are based on records or the latest Income Tax Statement Form received by the board.

CP 204 deferment

For CP204 payment, business criteria that qualify for the PMKS status are companies, cooperatives, trust bodies and limited liability partnerships with a paid-up capital of less than RM2.5 million for ordinary shares at the start of the basic period of an assessment year.

In addition, the entity’s gross business income of RM50 million or below for an assessment year.

The postponement of CP204 payment to the taxpayer who fulfils the criteria will be sent via registered email with HASiL (the IRB).

CP500 deferment

The IRB informed that the postponement of CP500 payment is allowed automatically to all taxpayers concerned for the 2021 assessment year payment (for the payable date of Jan 1, 2022) and the 2022 assessment year payment (for the payable dates of March 1, 2022 and May 1, 2022).

FAQ on deferment

Frequently asked questions (FAQ) on the postponement could be accessed via the link https://phl.hasil.gov.my/pdf/pdfam/SOALAN_LAZIM_PINDAAN_BAJET_2022_CP204.pdf and the public can contact the HASiL Recovery Call Centre (HRCC) at 03-8751 1000 for further information.

Visit Us

-

Wisma KTP, 53 Jalan Molek 1/8, Taman Molek, 81100 Johor Bahru

-

Wisma THK, 41, Jalan Molek 1/8, Taman Molek, 81100 Johor Bahru

KTP (Audit, Tax, Advisory)

An approved audit firm and licensed tax firm operating under the KTP group based in Johor Bahru providing audit, tax planning, advisory and compliance services to clients

-

Website www.ktp.com.my

-

Instagram https://bit.ly/3jZuZuI

-

Linkedin https://bit.ly/3sapf4l

-

Telegram http://bit.ly/3ptmlpn

THK (Secretarial, Account, Payroll, Advisory)

A licensed secretarial firm in Johor Bahru providing fast reliable incorporation, secretarial services, corporate compliance services, outsource booking, accounting and payroll services to clients

-

Website www.thks.com.my

-

Facebook https://bit.ly/3nQ98rs

KTP Lifestyle

An internal community for our colleagues on work and leisure.

-

Tiktok http://bit.ly/3u9LR6Q

-

Youtube http://bit.ly/3ppmjyE

-

Facebook http://bit.ly/3ateoMz

-

Instagram https://bit.ly/3jZpKLo

KTP Career

An external job community on vacancy in Johor Bahru for interns, graduates & experienced candidates.

-

Instagram https://bit.ly/3u2PxHg

-

Facebook http://bit.ly/3rPxz9o

#Ktp #Thks

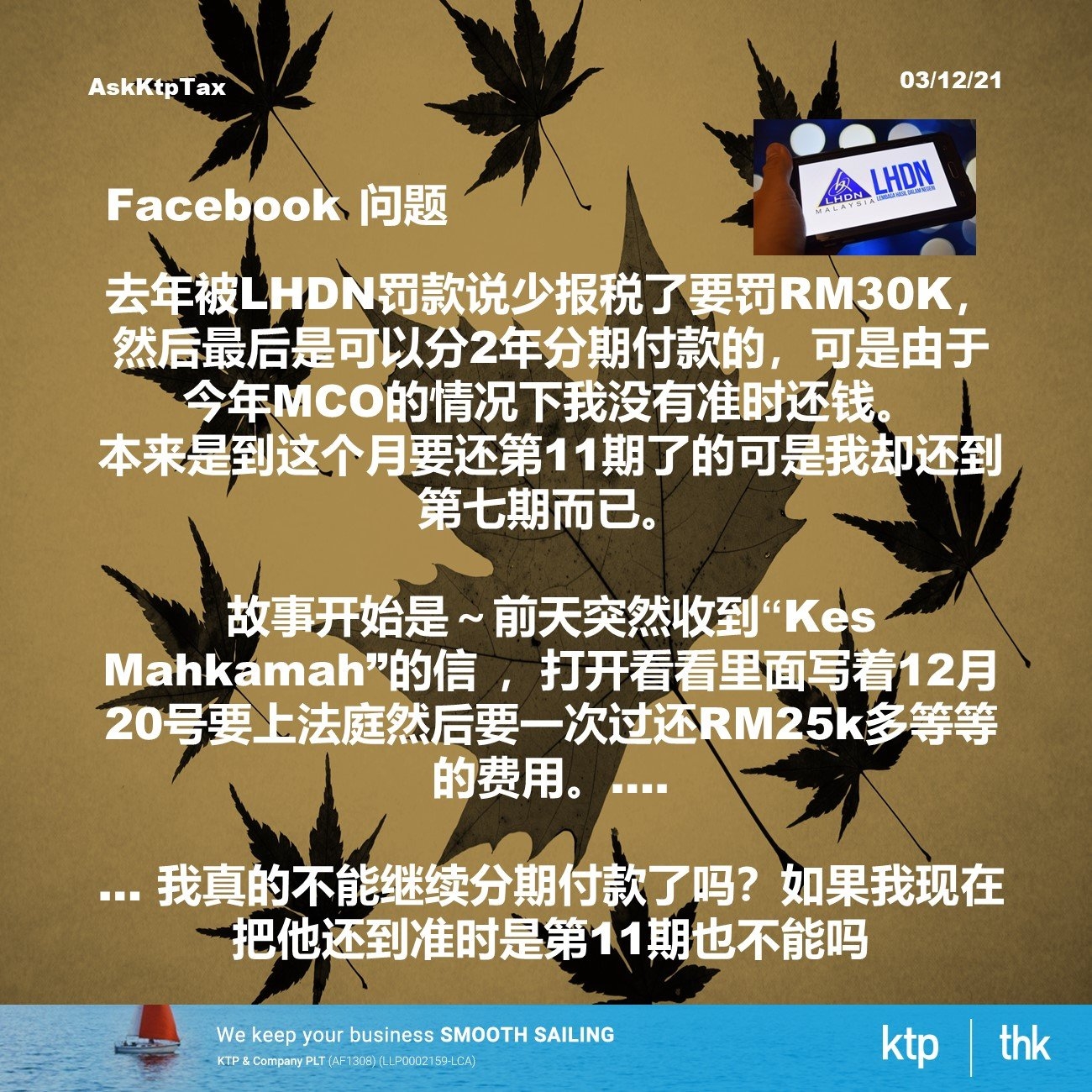

What is tax recovery action by LHDN?

What is tax recovery action by LHDN?

Background story from a Facebook post

Last year, I was fined by LHDN for under-declaring the tax and I was fined RM30K with 2 years instalments. Because of the MCO this year, I did not pay the money on time. Originally, it was the 11th issue this month, but I was only going to the seventh issue.…

I suddenly received a letter from ''Kes Mahkamah'' the day before yesterday. I opened it and saw that it said that I would go to court on December 20 and I had to pay more than RM25k in one go. ….…

Can I really continue to pay in instalments? Can't it be the 11th issue if I return him on time now?

LHDN tax recovery action

LHDN can file a recovery action against the taxpayer if no payment is made after 30 days from the services of the Notice of Assessment (NOA).

Judgement in Default

A writ saman (writ of summons) and pernyataan tuntutan (statement of claim) will be served to the taxpayer. If the taxpayer does not enter appearance within 14 days, a judgement in default of appearance (JID) will be entered against the taxpayer. Once a JID is entered, LHDN can proceed to execute the JID against the taxpayer.

Summary of Judgement

If summary judgement is entered, LHDN will proceed to file bankruptcy proceedings against taxpayer to recover the taxes. Once summary judgement is entered, taxpayer must by lumpsum. Thus, negotiate for instalment scheme before summary judgement is entered.

A summary judgement means a judgment can be entered against taxpayer without having to go for a trial. The Court will not entertain any challenges on the correctness of the assessment. The challenges can only be done at the Special Commission of Income Tax.

Instalment scheme S103(7) ITA 1967

Where any tax is payable in accordance with subsection (2), the Director General may allow the tax to be paid by instalments in such amounts and on such dates …. in the event of default in payment of any one instalment on the date specified for payment the balance of the tax then outstanding shall be due and payable on that date and shall without any further notice being served … and that sum shall be recoverable as if it were tax due and payable under this Act.

Consent Judgement

A consent judgment will be recorded before the Court when both parties (taxpayer and LHDN) agree to the instalment plan.

A lapse in any one of payment, the Consent Judgement will be revoked and the tax will become due and payable immediately.

No bankruptcy/winding-up proceeding will be filed against the taxpayer as long as payment is made.

Visit Us

-

Wisma KTP, 53 Jalan Molek 1/8, Taman Molek, 81100 Johor Bahru

-

Wisma THK, 41, Jalan Molek 1/8, Taman Molek, 81100 Johor Bahru

KTP (Audit, Tax, Advisory)

An approved audit firm and licensed tax firm operating under the KTP group based in Johor Bahru providing audit, tax planning, advisory and compliance services to clients

-

Website www.ktp.com.my

-

Instagram https://bit.ly/3jZuZuI

-

Linkedin https://bit.ly/3sapf4l

-

Telegram http://bit.ly/3ptmlpn

THK (Secretarial, Account, Payroll, Advisory)

A licensed secretarial firm in Johor Bahru providing fast reliable incorporation, secretarial services, corporate compliance services, outsource booking, accounting and payroll services to clients

-

Website www.thks.com.my

-

Facebook https://bit.ly/3nQ98rs

KTP Lifestyle

An internal community for our colleagues on work and leisure.

-

Tiktok http://bit.ly/3u9LR6Q

-

Youtube http://bit.ly/3ppmjyE

-

Facebook http://bit.ly/3ateoMz

-

Instagram https://bit.ly/3jZpKLo

KTP Career

An external job community on vacancy in Johor Bahru for interns, graduates & experienced candidates.

-

Instagram https://bit.ly/3u2PxHg

-

Facebook http://bit.ly/3rPxz9o

#Ktp #Thks

Special Tax Incentive under Penjana

Special Tax Incentive for Selected Services Activities under National Economic Recovery Plan (PENJANA)

The scope of Special Tax Incentive under the Economic Recovery Plan (PENJANA) is not only to assist manufacturing companies to relocate their operations to Malaysia. In Budget 2021, it also expanded to selected service activities, including companies adapting Industrial Revolution 4.0 and digitalization technology.

Key takeaways:

You will understand: -

1. Who is eligible for the tax incentive?

2. What are the tax incentives?

3. What are the selected service activities?

4. What are the key conditions to be fulfilled?

5. How to apply?

Summary of learnings:

1. Who is eligible for the tax incentive?

New company

A company that does not have:

a. any existing operation/entity in Malaysia with including the related company, or

b. any existing services operation in Malaysia but has an existing non-services operation, e.g. manufacturing

and is planning to:

a. Relocate its facility for qualifying services activities from any foreign country; or

b. Relocate new services activities; or

c. Establish new operation in Malaysia

Existing company

A foreign or locally owned company with existing services operation (including selected services activities) in Malaysia; and

Proposes to undertake selected services activities for a new business segment, which is separate from the operation of its existing services activities.

2. What are the tax incentives?

New company

-

Income tax rate: 0% to 10%

-

Period: up to 10 years.

Existing company

-

Income tax rate: 10%

-

Period: up to 10 years

3. What are the selected service activities?

The company must undertake any of the following service activities:

i. Provision of technology solutions based on substantial scientific or engineering challenges;

ii. Provision of Infrastructure and technology for cloud computing;

iii. Research and development/design and development activities;

iv. Medical devices testing laboratory and clinical trials; and

v. Any services or manufacturing-related services activities determined by the Minister of Finance

4. What are the key conditions to be fulfilled?

Some of the key conditions are outlined as below:

i. Company incorporated under Companies Act 2016 and resident in Malaysia;

ii. To commence business operation within one year from the date of approval;

iii. Incur the first capital expenditure within one year from the date of approval for the incentive and to be completed within three years from the date of the first capital expenditure was incurred; and

iv. To incur capital investment or business expenditure in the following areas:

a. Adoption of Industrial Revolution 4.0 or digitalisation technology;

b. Employment opportunities for Malaysians including fresh Malaysian graduates;

c. Technology transfer;

d. Utilization of local goods and services;

e. Internship for Malaysian students;

f. Collaboration with local industries/institutions/universities.

5. How to apply?

The completed application should be submitted in three (3) sets of PENJANA (Services) Form to MIDA before 31 December 2022.

Source:

https://www.mida.gov.my/wp-content/uploads/2021/09/Revised-Guideline-Relocation-Incentive_as-at-22.9.2021-for-MIDAs-website_final-v2.pdf

Visit Us

-

Wisma KTP, 53 Jalan Molek 1/8, Taman Molek, 81100 Johor Bahru

-

Wisma THK, 41, Jalan Molek 1/8, Taman Molek, 81100 Johor Bahru

KTP (Audit, Tax, Advisory)

An approved audit firm and licensed tax firm operating under the KTP group based in Johor Bahru providing audit, tax planning, advisory and compliance services to clients

-

Website www.ktp.com.my

-

Instagram https://bit.ly/3jZuZuI

-

Linkedin https://bit.ly/3sapf4l

-

Telegram http://bit.ly/3ptmlpn

THK (Secretarial, Account, Payroll, Advisory)

A licensed secretarial firm in Johor Bahru providing fast reliable incorporation, secretarial services, corporate compliance services, outsource booking, accounting and payroll services to clients

-

Website www.thks.com.my

-

Facebook https://bit.ly/3nQ98rs

KTP Lifestyle

An internal community for our colleagues on work and leisure.

-

Tiktok http://bit.ly/3u9LR6Q

-

Youtube http://bit.ly/3ppmjyE

-

Facebook http://bit.ly/3ateoMz

-

Instagram https://bit.ly/3jZpKLo

KTP Career

An external job community on vacancy in Johor Bahru for interns, graduates & experienced candidates.

-

Instagram https://bit.ly/3u2PxHg

-

Facebook http://bit.ly/3rPxz9o

#Ktp #Thks

KISB vs Ketua Pengarah Dalam Hasil Negeri

KISB vs Ketua Pengarah Dalam Hasil Negeri

Lesson from Tax Case : KISB vs Ketua Pengarah Dalam Hasil Negeri

1. Expenses incurred by the director (Company Vs Personal).

2. Wrong business code on 2nd business source.

Background information

The Company is operating a clinic.

The income generated from:

1. Consultancy fees and selling medicine for cure the patient.

2. Sales of supplement medicine to patients.

The Company discloses income separately for clinic income and supplement medicine in the tax computation.

Tax Issue 1 - Deductibility of “private” expenses

The Company incurred the following expenses:

- Training expenses,

- Repair,

- Service and maintenance; and

- General expenses.

Are these expenses allowable for tax deduction??

Tax Issue 2 : Wrong business code in tax computation

The Company discloses income separately for clinic income and supplement medicine

Does the presentation of tax computation use 2 business source of income is correct?

The Company’s opinion on Issue 1:

All the expenditures were basic expenses and a necessity in providing beneficial training to its patients as well as the buyers of the vitamin supplements allegedly sold by the Company.

1. All the expenditures were basic expenses and a necessity in providing beneficial training to its patients as well as the buyers of the vitamin supplements allegedly sold by the Company.

2. Presentation of tax computation is allowable as the principal activities include general traders and dealers.

The Company’s opinion on Issue 2:

Presentation of tax computation is allowable as the principal activities include general traders and dealers.

IRB argument on Issue 1:

The expenditures in question were not eligible for deduction under Section 33(1) of the ITA for the following reasons:

a) Expenses were not incurred by the Company but by one of its directors;

b) It was of personal expenses in nature; and

c) Expenses not supported by the relevant documentation.

IRB argument on Issue 2:

The income of “Business 2nd source - supplement medicine” was wrongly declared and reported by the Company as the income was from the multi-level-marketing (MLM) business of one of the Company’s directors

Therefore, it should be declared and reported separately from the Company’s income.

The decision by The Court

The Company expenses were not allowed for deduction due to the following reason:

1) Failed in proving that the expenses incurred are eligible for deduction under Section 33(1) of the ITA;

2) The Company had failed to call any witnesses to support its claim;

3) Failed to show that the expenditure is not capital in nature; and

4) The expenses incurred were found not related to the business of the Company.

Source:

https://phl.hasil.gov.my/pdf/pdfam/KISB_v_KPHDN_31012020.pdf

Visit Us

-

Wisma KTP, 53 Jalan Molek 1/8, Taman Molek, 81100 Johor Bahru

-

Wisma THK, 41, Jalan Molek 1/8, Taman Molek, 81100 Johor Bahru

KTP (Audit, Tax, Advisory)

An approved audit firm and licensed tax firm operating under the KTP group based in Johor Bahru providing audit, tax planning, advisory and compliance services to clients

-

Website www.ktp.com.my

-

Instagram https://bit.ly/3jZuZuI

-

Linkedin https://bit.ly/3sapf4l

-

Telegram http://bit.ly/3ptmlpn

THK (Secretarial, Account, Payroll, Advisory)

A licensed secretarial firm in Johor Bahru providing fast reliable incorporation, secretarial services, corporate compliance services, outsource booking, accounting and payroll services to clients

-

Website www.thks.com.my

-

Facebook https://bit.ly/3nQ98rs

KTP Lifestyle

An internal community for our colleagues on work and leisure.

-

Tiktok http://bit.ly/3u9LR6Q

-

Youtube http://bit.ly/3ppmjyE

-

Facebook http://bit.ly/3ateoMz

-

Instagram https://bit.ly/3jZpKLo

KTP Career

An external job community on vacancy in Johor Bahru for interns, graduates & experienced candidates.

-

Instagram https://bit.ly/3u2PxHg

-

Facebook http://bit.ly/3rPxz9o

#Ktp #Thks

Stamp duty exemption 2021

Stamp duty exemption 2021

How to save stamp duty with our Government exemption order during this pandemic?

Two exemption orders:

1. Stamp duty (Exemption) (No. 10) Order 2021 [P.U.(A) 364/2021].

Stamp duty exemption on the instrument of loan or financing agreement executed between a Small and Medium Enterprise (SME) and a financial institution

Stamp Duty (Exemption) (No. 10) Order 2021 [P.U.(A) 364/2021] was gazetted on 10 September 2021 and was deemed to have come into operation and effective on 1 January 2021.

The Order provides that the exemption shall apply to relevant instruments executed under a letter of offer issued by the Financial Institution to a SME between 01 January 2021 to 31 December 2021.

Loan or financing facility approved under Bank Negara Malaysia (BNM)’s Fund for SMEs:

(i) All Economic Sectors Facility

(ii) Small Medium Enterprises Automation and Digitalization Facility;

(iii) Agrofood Facility

*An Application must be submitted for the exemption

2. Stamp duty (Exemption) (No.11) Order 2021 – [P.U.(A) 367/2021]

Stamp duty exemption on qualifying loan restructuring and rescheduling agreements.

Stamp duty (Exemption) (No.11) Order 2021 – [P.U.(A) 367/2021] was gazetted on 15 September 2021 and was deemed to have come into operation and effective on 1 July 2021.

This new order is to extend the exemption period under Stamp Duty (Exemption)(No.2) Order 2020 [P.U.(A) 165/2020].

The Amendment Order provides that:

This exemption applies to the loan restructuring and rescheduling agreements executed on or after 01 July 20201 to 31 December 2021. (previously until 30 June 2021)

The exemption is subject to the following conditions: -

1. An application must be submitted for the exemption;

2. The existing loan and financing agreement has duly stamped under item 22 or 27 of the First Schedule to the Act;

3. Do not contain any additional value to the original amount of loan or financing agreement relating to the restructuring or rescheduling of a loan of financing;

4. Any interest or profit accrued from the restructured or rescheduled payments is not considered as an element of additional value.

Source:

i. Stamp duty exemption on the instrument of loan or financing agreement

ii. Stamp duty exemption on the instrument of loan or financing agreement executed between a Small and Medium Enterprise (SME) and a financial institution

Visit Us

-

Wisma KTP, 53 Jalan Molek 1/8, Taman Molek, 81100 Johor Bahru

-

Wisma THK, 41, Jalan Molek 1/8, Taman Molek, 81100 Johor Bahru

KTP (Audit, Tax, Advisory)

An approved audit firm and licensed tax firm operating under the KTP group based in Johor Bahru providing audit, tax planning, advisory and compliance services to clients

-

Website www.ktp.com.my

-

Instagram https://bit.ly/3jZuZuI

-

Linkedin https://bit.ly/3sapf4l

-

Telegram http://bit.ly/3ptmlpn

THK (Secretarial, Account, Payroll, Advisory)

A licensed secretarial firm in Johor Bahru providing fast reliable incorporation, secretarial services, corporate compliance services, outsource booking, accounting and payroll services to clients

-

Website www.thks.com.my

-

Facebook https://bit.ly/3nQ98rs

KTP Lifestyle

An internal community for our colleagues on work and leisure.

-

Tiktok http://bit.ly/3u9LR6Q

-

Youtube http://bit.ly/3ppmjyE

-

Facebook http://bit.ly/3ateoMz

-

Instagram https://bit.ly/3jZpKLo

KTP Career

An external job community on vacancy in Johor Bahru for interns, graduates & experienced candidates.

-

Instagram https://bit.ly/3u2PxHg

-

Facebook http://bit.ly/3rPxz9o

#Ktp #Thks

Accounting for bitcoin (cryptocurrency)

Accounting for bitcoin (cryptocurrency)

No accounting standard currently exists to explain how cryptocurrency should be accounted for, accountants have no alternative but to refer to existing accounting standards.

What is cryptocurrency?

Cryptocurrency is an intangible digital token that is recorded using a distributed ledger infrastructure, often referred to as a blockchain.

These tokens provide various rights of use. For example, cryptocurrency is designed as a medium of exchange. Other digital tokens provide rights to the use other assets or services, or can represent ownership interests.

These tokens are owned by an entity that owns the key that lets it create a new entry in the ledger. Access to the ledger allows the re-assignment of the ownership of the token. These tokens are not stored on an entity’s IT system as the entity only stores the keys to the Blockchain (as opposed to the token itself).

They represent specific amounts of digital resources which the entity has the right to control, and whose control can be reassigned to third parties

What accounting standards

Cash & cash equivalents

Bitcoin is too volatile! Cash is readily convertible to known amounts of cash and which are subject to an insignificant risk of changes in value.

Financial assets

It does not represent cash, an equity interest in an entity, or a contract establishing a right or obligation to deliver or receive cash or another financial instrument.

Moreover, bitcoins do not provide the holders with a residual interest in the assets of an entity after deducting all its liabilities.

Property, Plant & Equipment

Bitcoin is not a tangible asset so it does not fall into the scope of PPE.

Inventory

Inventory accounting may be appropriate if an entity holds bitcoins for sale in the ordinary course of business.

However if an entity holds bitcoins for investment purposes over a period of time, inventory accounting is not appropriate.

Intangible assets

It appears to meet the definition of an intangible asset which define as an identifiable non-monetary asset without physical substance.

Visit Us

-

Wisma KTP, 53 Jalan Molek 1/8, Taman Molek, 81100 Johor Bahru

-

Wisma THK, 41, Jalan Molek 1/8, Taman Molek, 81100 Johor Bahru

KTP (Audit, Tax, Advisory)

An approved audit firm and licensed tax firm operating under the KTP group based in Johor Bahru providing audit, tax planning, advisory and compliance services to clients

-

Website www.ktp.com.my

-

Instagram https://bit.ly/3jZuZuI

-

Linkedin https://bit.ly/3sapf4l

-

Telegram http://bit.ly/3ptmlpn

THK (Secretarial, Account, Payroll, Advisory)

A licensed secretarial firm in Johor Bahru providing fast reliable incorporation, secretarial services, corporate compliance services, outsource booking, accounting and payroll services to clients

-

Website www.thks.com.my

-

Facebook https://bit.ly/3nQ98rs

KTP Lifestyle

An internal community for our colleagues on work and leisure.

-

Tiktok http://bit.ly/3u9LR6Q

-

Youtube http://bit.ly/3ppmjyE

-

Facebook http://bit.ly/3ateoMz

-

Instagram https://bit.ly/3jZpKLo

KTP Career

An external job community on vacancy in Johor Bahru for interns, graduates & experienced candidates.

-

Instagram https://bit.ly/3u2PxHg

-

Facebook http://bit.ly/3rPxz9o

#Ktp #Thks

Public Ruling (PR) No. 4/2021: Taxation of Income Arising from Settlements

Public Ruling (PR) No. 4/2021: Taxation of Income Arising from Settlements

The IRB has published Public Ruling (PR) No. 4/2021: Taxation of Income Arising from Settlements, dated 13 August 2021.

The objective of Public Ruling 4/2021

The PR explains the taxation of income arising from a settlement created by a person for the benefit of another person.

* Clarify who constitutes a “settlor” and what constitute “settlements” for income tax purposes

• Explain the circumstances where income arising from a settlement is deemed to be the income of a settlor and hence assessable on him/her.

• Explain how the amount of income of a settlor from settlements is determined

• Explain the tax treatment in a settlement where there are two or more settlors

Example

Mr Rich transferred a shophouse to his unmarried son as a gift for his 18 years old birthday. The shophouse will generate RM10,000 of rental income every month.

The rental income should be assessable under Mr Rich or his son?

The rental income would be deemed to be Mr Rich’s income, as his son is below 18 years old and unmarried.

When his son attains 21 years old, the rental income would be assessable under his son.

But why?

Because there is a “settlement” for an unmarried relative under 21 years of age.

Definition of settlement in tax ruling

In a settlement, there must be an element of giving or getting something for nothing or less than the open market value.

The shophouse is treated as a birthday gift to his son without any consideration.

Tax treatment on income from the settlement

In subsection 65 of ITA mentions that the settlement for an unmarried relative under 21 years’ old, income would be deemed to be the income of settlor (Mr Rich) where a settlement is created either directly or indirectly for the benefit of a relative.

However, in subsection 65(1) of ITA, the income would be deemed as income of the relative when:

1. in the event of the death of the settlor;

2. a relative under 21 years old who is married;

3. a relative who is 21 years old and above whether married or unmarried.

In this case, his son is unmarried and 18 years old.

Source:

PR4/2021 – Taxation of income arising from settlements: https://phl.hasil.gov.my/pdf/pdfam/PR_04_2021.pdf

Section 65 of Income Tax Act 1967 - https://phl.hasil.gov.my/pdf/pdfam/Act_53.pdf

Visit Us

-

Wisma KTP, 53 Jalan Molek 1/8, Taman Molek, 81100 Johor Bahru

-

Wisma THK, 41, Jalan Molek 1/8, Taman Molek, 81100 Johor Bahru

KTP (Audit, Tax, Advisory)

An approved audit firm and licensed tax firm operating under the KTP group based in Johor Bahru providing audit, tax planning, advisory and compliance services to clients

-

Website www.ktp.com.my

-

Instagram https://bit.ly/3jZuZuI

-

Linkedin https://bit.ly/3sapf4l

-

Telegram http://bit.ly/3ptmlpn

THK (Secretarial, Account, Payroll, Advisory)

A licensed secretarial firm in Johor Bahru providing fast reliable incorporation, secretarial services, corporate compliance services, outsource booking, accounting and payroll services to clients

-

Website www.thks.com.my

-

Facebook https://bit.ly/3nQ98rs

KTP Lifestyle

An internal community for our colleagues on work and leisure.

-

Tiktok http://bit.ly/3u9LR6Q

-

Youtube http://bit.ly/3ppmjyE

-

Facebook http://bit.ly/3ateoMz

-

Instagram https://bit.ly/3jZpKLo

KTP Career

An external job community on vacancy in Johor Bahru for interns, graduates & experienced candidates.

-

Instagram https://bit.ly/3u2PxHg

-

Facebook http://bit.ly/3rPxz9o

#Ktp #Thks

Tax estimation LHDN 2022

MyTax: LHDNM

MyTax: LHDNM

2021 最佳 app - MyTax. 一旦安装 MyTax, 不陷入任何骗局.

这是一个方便纳税人查看税务的软件, 你就可以查询并使用更多相关的税务服务。

-

所得税官网

-

税务呈报

-

电子盖章系统

-

线上呈报薪酬资料

-

预扣税计算机

-

资料更新

-

税务分类账

-

税务居民

-

税务清关

-

印花税

只要点击分类账, 你就可以查询自己有没有拖欠的税务, 并查询有关的税务估算表(CP500).

这个软件有什么好处呢?

-

纳税人能更方便的查询个人的税收信息。

-

节省时间,成本和交通,无需去LHDNM柜台询问税收信息,因为一切都触手可及

-

允许用户使用一个用户名(ID)和密码登录到多个相关软件系统,并使用LHDNM所提供的其他服务.

How to 下载

-

安卓用户可以通过 google play store下载

-

苹果用户可以通过 app store下载

Visit Us

-

Wisma KTP, 53 Jalan Molek 1/8, Taman Molek, 81100 Johor Bahru

-

Wisma THK, 41, Jalan Molek 1/8, Taman Molek, 81100 Johor Bahru

KTP (Audit, Tax, Advisory)

An approved audit firm and licensed tax firm operating under the KTP group based in Johor Bahru providing audit, tax planning, advisory and compliance services to clients

-

Website www.ktp.com.my

-

Instagram https://bit.ly/3jZuZuI

-

Linkedin https://bit.ly/3sapf4l

-

Telegram http://bit.ly/3ptmlpn

THK (Secretarial, Account, Payroll, Advisory)

A licensed secretarial firm in Johor Bahru providing fast reliable incorporation, secretarial services, corporate compliance services, outsource booking, accounting and payroll services to clients

-

Website www.thks.com.my

-

Facebook https://bit.ly/3nQ98rs

KTP Lifestyle

An internal community for our colleagues on work and leisure.

-

Tiktok http://bit.ly/3u9LR6Q

-

Youtube http://bit.ly/3ppmjyE

-

Facebook http://bit.ly/3ateoMz

-

Instagram https://bit.ly/3jZpKLo

KTP Career

An external job community on vacancy in Johor Bahru for interns, graduates & experienced candidates.

-

Instagram https://bit.ly/3u2PxHg

-

Facebook http://bit.ly/3rPxz9o

#Ktp #Thks

Certificate of Residence LHDN

Do you know how to reduce withholding tax with the certificate of residence (COR)?

A certificate of Residence (COR) is issued to confirm the residence status of the taxpayer.

Objectives of COR

-

Claim tax benefits under the Double Taxation Agreement (DTA).

-

Avoid double taxation on the same income.

COR is specifically for Malaysia’s treaty partners only.

Application of COR

Application for COR can be made either manually or can be made through e-Residence (https://eresidence.hasil.gov.my/).

The COR will be ready within 10 working days with the fully duly required

documents and information furnished.

Final words

Further information on COR can be obtained from the IRBM Official Portal at

www.hasil.gov.my > International > Certificate of Resident

Visit Us

-

Wisma KTP, 53 Jalan Molek 1/8, Taman Molek, 81100 Johor Bahru

-

Wisma THK, 41, Jalan Molek 1/8, Taman Molek, 81100 Johor Bahru

KTP (Audit, Tax, Advisory)

An approved audit firm and licensed tax firm operating under the KTP group based in Johor Bahru providing audit, tax planning, advisory and compliance services to clients

-

Website www.ktp.com.my

-

Instagram https://bit.ly/3jZuZuI

-

Linkedin https://bit.ly/3sapf4l

-

Telegram http://bit.ly/3ptmlpn

THK (Secretarial, Account, Payroll, Advisory)

A licensed secretarial firm in Johor Bahru providing fast reliable incorporation, secretarial services, corporate compliance services, outsource booking, accounting and payroll services to clients

-

Website www.thks.com.my

-

Facebook https://bit.ly/3nQ98rs

KTP Lifestyle

An internal community for our colleagues on work and leisure.

-

Tiktok http://bit.ly/3u9LR6Q

-

Youtube http://bit.ly/3ppmjyE

-

Facebook http://bit.ly/3ateoMz

-

Instagram https://bit.ly/3jZpKLo

KTP Career

An external job community on vacancy in Johor Bahru for interns, graduates & experienced candidates.

-

Instagram https://bit.ly/3u2PxHg

-

Facebook http://bit.ly/3rPxz9o

#Ktp #Thks